This page is designed to assist providers in the completion of the Survey of International Investment Form 90, Form 52D and 53D. The Survey of International Investment is the main source of data for official statistics on foreign investment in Australia, Australian investment abroad and foreign debt.

The results of this survey are used in the compilation of Australia’s Balance of Payments and International Investment Position each quarter.

This booklet is compiled in accordance with the International Monetary Fund’s Balance of Payments and International Investment Position Manual, Sixth Edition.

Notes

These notes are divided into several parts as follows:

1. Reporting arrangements

1.1 Form 90, The Survey of International Investment

Form 90, The Survey of International Investment, collects information about the financial claims and liabilities to non-residents, held or managed by Australian corporations and Australian branches of foreign corporations.

An Australian enterprise group consists of an Australian parent enterprise (the top Australian enterprise), its Australian branches and its Australian subsidiaries as defined by the Corporations Law.

Form 90 should be completed by the top Australian enterprise for a single institutional sub-sector. The claims and liabilities of majority owned subsidiaries and branches should be consolidated with those of the top enterprise of that sector, with the exception of Equity liabilities in Parts A and B.

1.2

A separate Form 90 should be completed for each group of enterprises within your Australian enterprise group according to their institutional sub-sector.

These are:

- Banks

- Other depository corporations (see Note 1.4)

- Life insurance and pension funds

- Other insurance corporations

- Money market funds (see Note 1.5)

- Non-money market financial investment funds (see Note 1.6)

- Securitisers (see Note 1.7)

- Other financial institutions

- Trading enterprises, non-financial corporations. (see Note 1.9)

Groups spanning more than one institutional sub-sector need to complete separate forms for each of those sub-sectors.

For example, if your group’s top enterprise is predominantly engaged in licensed banking activities and also has non-bank depository subsidiaries and investment funds management subsidiaries, three Form 90s should be completed, covering:

- All the Australian enterprises within your enterprise group that are licensed banks.

- All the Australian enterprises within your enterprise group which are non- bank depository corporations.

- All the Australian enterprises within your enterprise group which are investment funds managers.

If your enterprise group extends beyond one institutional sub-sector and appropriate reporting arrangements have not already been negotiated with the ABS, please contact the ABS on the number listed on the front page of Form 90.

1.3 Financial intermediaries

Financial intermediaries, for the purpose of Form 90, consist of banks, other depository corporations, investment funds and securitisers.

1.4 Other depository corporations

Other depository corporations are those non-bank financial intermediaries with liabilities included in The Reserve Bank of Australia’s definition of broad money. This includes those financial corporations registered in categories A to G of the Financial Corporations Act and cash management trusts.

1.5 Money market investment funds

Money market investment funds are collective investment schemes that raise funds by issuing shares or units to the public, either via a prospectus or a distribution channel such as a platform. The proceeds are used primarily to invest in money market instruments such as short term debt securities, bank deposits and other investments with similar yields.

1.6 Non-money market investment funds

Non-money market investment funds are collective investment schemes which raise funds by issuing shares or units to the public, either via a prospectus or a distribution channel such as a platform.

The proceeds are used to purchase financial assets, which are owned by the investment fund. Investors are able to dispose of their shares on well developed secondary market, such as a stock exchange or through readily accessible redemption facilities. For the reporting arrangements for funds managers, see Note 2.

Including

- Pooled funds

- Master trusts

- Hedge funds

- Wholesale trusts

- Funds with predominantly overseas property or infrastructure holdings

- Listed and unlisted equity trusts, infrastructure trusts and mortgage trusts

- Listed investment companies

Excluding

- Funds managed under an individual mandate

- Pension funds

1.7 Securitisers

Securitisers are entities which pool various types of assets such as residential mortgages, commercial property loans and credit card debt. These are then packaged and used as collateral backing for bonds or short-term debt securities, referred to asset backed securities, which are then sold to investors.

1.8 Other financial institutions

Other financial institutions include financial intermediaries not already classified above. This includes commercial financiers and co-operative housing societies.

1.9 Corporate trading enterprises

Corporate trading enterprises are corporations whose principal activity is the production of market goods or non-financial services.

1.10

Throughout this form you are asked to record separately your liabilities to and claims on:

- Your non-resident direct investors (see Note 3.2)

- Your direct investment groups abroad, (see Note 3.3)

- Your non-resident fellow enterprises (see Note 3.4)

- Other non-resident investors

Including

- All financial liabilities to or claims on non-residents which are shown in your books

- Activities of your offshore banking units (OBUs)

- Activities of resident pooled investment funds managed by your Australian enterprise group (see Note 2)

- Investments abroad which are being managed on behalf of your Australian enterprise group by an independent investment manager in Australia via an individual mandate (see Note 2)

Excluding

- Financial liabilities and assets which your Australian enterprise group has negotiated on behalf of others and which are not shown in your books, except in those cases described above

- Claims and liabilities to Australian residents denominated in foreign currency

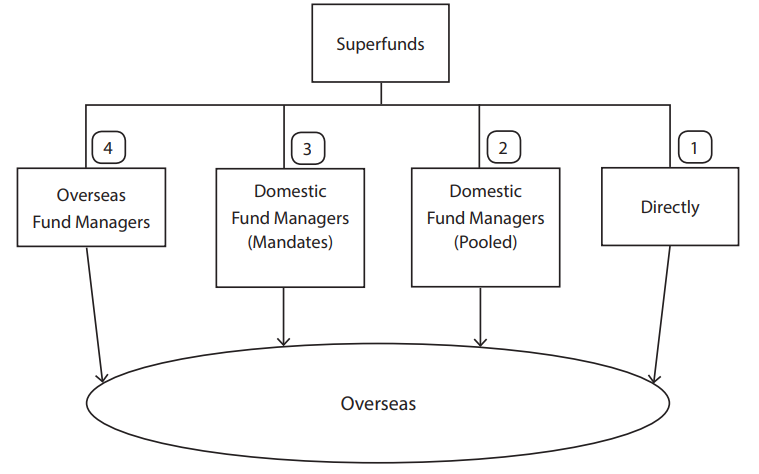

2. Funds under management and funds managed on your behalf

This diagram illustrates reporting requirements for different types of investment flows for funds under management and funds managed on your behalf. Please note that superannuation funds are used as an example but it could include entities such as Life or General Insurance.

We expect superannuation funds to report their overseas investment in the case of investment scenarios 1, 3 and 4; whereas investment scenario 2 should be reported by fund managers.

Pooled investment funds are vehicles where the funds of multiple investors are aggregated to form a single portfolio. Funds placed in non-resident pooled investment funds should be included as equity claims on non-residents in Question 15 in the other non-resident counterparties segment if invested in equities, which includes unit, property and infrastructure trusts. If funds are invested in other instruments report these non-resident assets in the appropriate questions throughout the form.

Funds under management and funds managed on your behalf, where the funds are placed in a resident pooled investment fund and are managed by a resident fund manager, should not be included in Form 90.

The assets and liabilities arising from funds placed with fund managers should be included if they are managed by an individual mandate. Report these nonresident assets and liabilities managed by the fund manager on your behalf in the appropriate questions throughout the form.

Fund managers should not report funds under individual mandates.

Sources of funds from non-resident investors into resident fund management vehicles should be reported by the fund manager in Question 2 in the other nonresident investors segment of the question.

3. Key Concepts

3.1 Residents and non-residents

A resident is any individual, enterprise or other organisation ordinarily domiciled in Australia or its external territories, including Norfolk Island.

- Australian registered branches and incorporated subsidiaries of foreign enterprises are regarded as Australian residents.

A non-resident is any individual, enterprise or other organisation ordinarily domiciled in a country other than Australia.

- Foreign branches and foreign subsidiaries of Australian enterprises are regarded as non-residents.

3.2 Direct investors

Direct investors are non-residents (individuals, enterprises or groups of related individuals or enterprises) that hold 10% or more of the ordinary shares or voting stock of any Australian enterprise in your group. For Australian branches of non-resident enterprises, the non-resident direct investor is the head office of the branch.

Report the claims and liabilities relating to your non-resident direct investors separately from other counterparties where requested.

3.3 Direct investment groups abroad

Direct investment groups abroad comprise non-resident direct investment enterprises, non-resident branches and non-resident fellow enterprises of your Australian enterprise group. This consists of:

- Non-resident subsidiaries, where your Australian enterprise group holds 50% or more of the voting stock or ordinary shares.

- Non-resident associates, where your Australian enterprise group holds 10% or more, but less than 50% of the voting stock or ordinary shares.

- Your subsidiary’s non-resident subsidiaries and associates.

- Your associate’s non-resident subsidiaries, but not the associates of your associates.

For a more detailed explanation of these concepts, see Appendix 1.

Non-resident branches of an Australian enterprise group are the foreign offices of an Australian enterprise which are not separately incorporated abroad, as well as foreign offices of an unincorporated enterprise whose head office is in Australia. (Joint ventures and partnerships with non-residents are treated as foreign branches).

Report the claims and liabilities relating to your direct investment groups abroad separately from other counterparties where requested

3.4 Fellow enterprises

Fellow enterprises are non-resident enterprise groups which have the same direct investor as your Australian enterprise group. This means the foreign subsidiaries, associates or branches of your non-resident direct investors, where:

- These foreign enterprises hold less than 10% of the ordinary shares or voting stock in your Australian enterprise group; and

- Your Australian enterprise group holds less than 10% of the ordinary shares or voting stock in the foreign enterprises.

For example, a non-resident parent may have subsidiaries in multiple countries in which the Australian enterprise group has no equity holdings or liabilities. These non-resident subsidiaries would be considered fellow enterprises of your Australian enterprise group. For more detail, see Appendix 1.

Report the claims and liabilities relating to your non-resident fellow enterprises separately from other counterparties where requested.

3.5 Country of the non-resident counterparty

Country of the non-resident counterparty refers to the country in which the immediate non-resident creditor or debtor resides. However, it is not necessary to show separate details in respect of small values. If the opening and closing positions for particular countries are less than $A5 million, the amounts relating to these countries may be aggregated and attributed only to the country of the largest contributor within this group.

Note

- For international capital markets (e.g. Eurobond, Asian dollar issues) show the particular capital market as the country of the foreign creditor or debtor; and

- For syndicated borrowing, show details classified by the country of each syndicate member.

3.6 Opening and closing positions

Opening and closing positions refer to the stock of financial liabilities to and claims on non-residents by your Australian enterprise group at the beginning and end of the quarter respectively. The reported opening positions must agree with the closing positions reported in the previous quarter.

All valuations should be market valuations, or if not available, estimated using one of the suggested methods applicable to the instrument as defined throughout the Explanatory notes to accompany Form 90.

All values should be reported in thousands of Australian dollars. Positions denominated in foreign currency should be converted to Australian dollars at exchange rates applicable on the reference dates.

3.7 Transactions increasing or decreasing assets or liabilities to non-residents

Transactions increasing or decreasing assets or liabilities to non-residents consist of :

- The issuance of financial assets or creation of financial positions stock in your Australian enterprise group; and

- The redemption or maturity of financial assets or positions, and

- The purchase or sale of financial assets

Transactions should be recorded at the traded price and converted to Australian dollars by using the exchange rate applicable at the time of the transaction. Transactions should be recorded on a gross basis, before the deduction of commissions, brokerage fees and withholding taxes.

3.8 Market price changes

Market price changes refer to the impact on the value of the stock of financial liabilities and assets due to changes in their price excluding any exchange rate movements. Market price changes include both realised and unrealised gains or losses during the reporting period arising from:

- Interest rate movements

- Share price movements (listed enterprises)

- The impact of retained earnings or other revaluations (unlisted enterprises).

Market price changes should be estimated by marking to market where possible.

3.9 Exchange rate variations

Exchange rate variations refer to the impact on the stock of financial liabilities and assets due to changes in the exchange rate between the Australian dollar and other currencies in which these assets and liabilities are denominated.

3.10 Other changes

Other changes refers to changes to the stock of financial liabilities and assets not due to transactions, market price changes and exchange rate variations, and may include reclassifications (such as from portfolio to direct investment when the 10% equity threshold is reached), and debt write-offs.

3.11 Dividends

Dividends refers to all dividends that are recorded at your books close date, whether or not they are payable or actually paid in that quarter.

3.12 Operating profits

Operating profits should represent the net of operating revenues and costs. This differs from the concept of Profit in an accounting sense.

Including

- Operating income and expenses such as, but not limited to, interest revenue and expense, rents, wages, commissions, service fees, insurance premiums and claims, management fees and penalties for payments arrears

- Declared dividends received or to be received from other enterprises

- Any operating income exempt from taxation

- Provisions for depreciation, annual leave, unconditional long-service leave, employer contributions to superannuation, workers compensation and termination, retrenchment or redundancy payments

Excluding

- Capital gains and losses, both realised and unrealised

- Foreign exchange gains and losses

- Previous quarter’s losses

- Accelerated depreciation provisions for taxation purposes. Instead, the amount of depreciation should be calculated at current replacement costs

- Goodwill amortised

- Provisions for bad or doubtful debts

- Other provisions except those listed under Including above

- Dividends paid to investors

A net loss should be shown as a negative profit item.

Mining exploration expenditure should be capitalised, and depreciated as an expense each quarter using the average service lines used in your accounts.

3.13 Remitted profits

Remitted profits are the earnings that branches and other unincorporated enterprises remit to their head office. Remittances of profit during the quarter should be reported regardless of whether the profits were earned in respect of current or previous quarter activities.

3.14 Interest payable/receivable

Interest payable/receivable refers to interest income on debt securities that became contractually due for payment during the quarter, converted to Australian dollars using the exchange rate on the day the interest becomes due for payment.

Excluding

- Accruals of interest that become due for payment in subsequent quarters

- Discounts and premiums expensed during the quarter

- Discounts payable at maturity or on redemption of the security

3.15 Interest accrued

Interest accrued refers to interest income which accrued during the quarter on non-tradable instruments (that is, on trade credits, loans, deposits, and other claims and liabilities other than securities). Accrued interest should be converted to Australian dollars using the exchange rate on the last day of the period.

For loans and deposits where interest accrued contributes to the balance of the account rather than being paid out, interest accrued should have a corresponding transaction increasing the closing position

3.16

Residual maturity of financial assets or liabilities cross-classified by currency

Residual maturity (of the closing positions for the quarter) refers to the time remaining until an asset or liability is due to be fully repaid.

Currency (of the closing positions) refers to the currency in which the assets or liabilities are likely to be repaid. Positions denominated in foreign currency should be converted to Australian dollars. All values should be reported in thousands of Australian dollars ($A,000).

3.17 Long-term

Long-term refers to assets and liabilities with an original contractual maturity of more than one year. Assets and liabilities with an original contractual maturity of one year or less are classified as short-term.

3.18 Treatment of hedges

Financial instruments that are hedged by the use of derivatives (such as swaps and forward rate agreements) should be recorded according to the terms of the original contract and without regard to the hedge.

The details of the hedge, if it is with a non-resident counterparty, should be reported as derivative liabilities in Question 5 or derivative claims in Question 16, as appropriate.

For example, for a loan that is the subject of a swap, information on the underlying position, principal repayments and interest should be recorded in the appropriate columns in the loans question. The market value of the swap and the actual payments on the swap agreement should be recorded under the appropriate derivatives questions.

Section 1: Liabilities to non-residents

Part A Equity in and profit of the top Australian enterprise

A1 Equity

Equity refers to:

- All classes of shares or units on issue which are held by non-residents,

- The net equity held in:

- Australian branches of non-resident companies, and

- Joint ventures and other unincorporated enterprises.

Excluding

- Equity held by the Australian office of a nominee on behalf of non-residents

- Non-participating preference shares (see Note A8)

A2 Direct investment equity held by non-residents in the top Australian enterprise

Direct Investors refers to those non-residents who hold 10% or more of the equity of the top Australian enterprise, for example, offshore parents. (see Note 3.2).

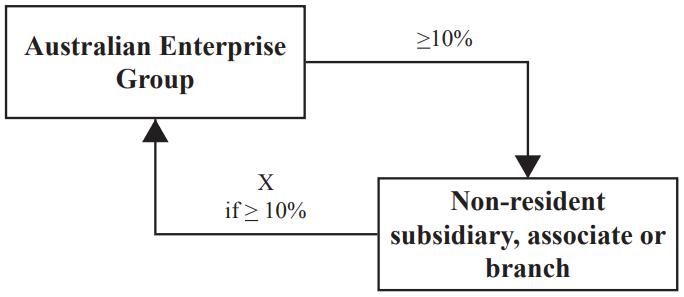

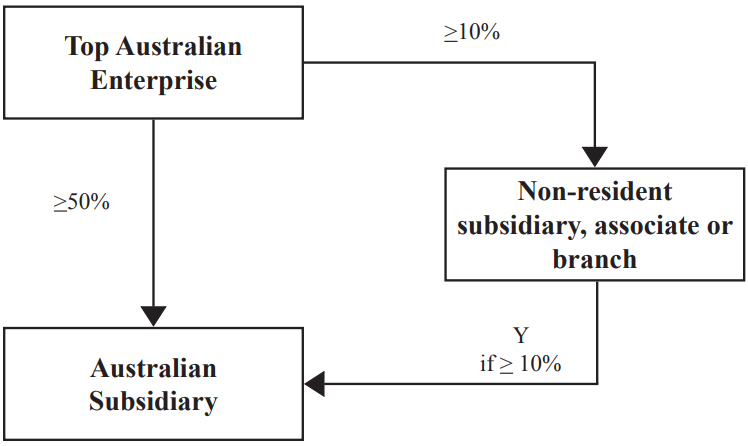

Direct investment groups abroad in Question 1a refers to your Australian subsidiaries and associates which also hold 10% or more of the ordinary shares or voting stock in your Australian Enterprise group. For example, all X values in Diagram 1. Equity holdings less than 10% should be reported in Question 2.

Diagram 1 - Holdings of ordinary shares or voting stock

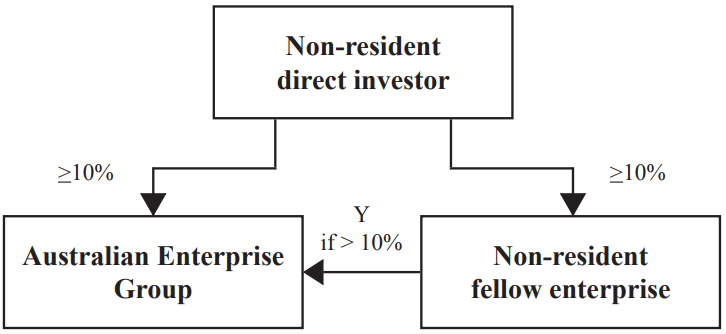

Fellow enterprises in Question 1a refers to non-resident fellow enterprises that hold ordinary shares or voting stock in your Australian enterprise group. For example, report all Y values in Diagram 2. The holding by a fellow enterprise cannot be greater than 10% of the ordinary shares or voting stock – this would be considered Direct Investment and should be reported above.

Diagram 2 - Holdings of ordinary shares or voting stock

A3 Transactions that increase or decrease your equity liabilities to non-residents.

Including

- Purchases or sales of shares in your enterprise group by non-residents

- Non-bonus issues, including calls and dividends re-invested

- Redemptions of your enterprise’s shares by non-residents

- Additions and withdrawals of equity capital by head office

Excluding

- Dividends paid to shareholders or parents

- Remitted profits (see Note 3.13)

A4 Market value of equity

For listed enterprises, equity positions should be reported using the market price on the reference date.

For unlisted enterprises, if a market price is not available, please estimate the market value of your shares by using one of the following methods, which are listed in order of preference:

- A recent transaction price

- Director’s valuation

- Net asset value

Net asset value is equal to total assets less non-equity liabilities, including intangibles. Assets and liabilities should be recorded at estimated market value, rather than historical values.

For net equity of a branch, joint venture or other unincorporated enterprise, report the total assets of the branch valued at current cost, less non-equity liabilities. Equity liabilities include retained earnings revaluation and other reserves, as well as capital invested by the head office.

A5 Tax payable

Tax payable on income earned during the quarter is an estimate of the amount of gross tax payable on income earned in the quarter, less any tax credits utilised in the quarter. Do not credit the taxation benefit of a current quarter loss.

A6 Other equity held by non-residents

Other equity held by non-residents refers to holdings of less than 10% of the equity in the top Australian enterprise.

Including

- The source of funds for pooled investment funds managed by your Australian Enterprise Group (see Note 2)

- Non-residents on the shareholder register of the Australian enterprise group

A7 Equity in the form of securities

Equity in the form of securities refers to any equity that is denominated in the form of listed or unlisted securities. This qualification is only relevant where the equity holding is less than 10% of the voting rights of the enterprise.

A8 Non-participating preference shares

Non-participating preference shares are a type of preference share where the holder has no entitlement to a share in the residual value on the dissolution of the issuing entity. Non-participating preference shares should be reported as ‘Longterm debt securities’ (Question 7).

Part B Outside equity held by non-resident investors

B1 Outside equity

Outside equity refers to equity held by non-residents in the partially owned subsidiaries of your Australian enterprise group.

A separate sheet should be completed for each Australian subsidiary with nonresident investors. Please call the ABS on the number on the Front Page of Form 90 if this is required.

B2 Direct investment equity held by non-residents in this Australian subsidiary

Direct investment equity held by non-residents in this Australian subsidiary refers to counterparties with equity holdings of 10% or greater of the ordinary shares or voting stock of the subsidiary, divided into three categories below.

Direct investors in Question 3a refers to any non-resident counterparty holding 10% or more of the ordinary shares or voting stock in any Australian enterprise in your group. For example, report all X values in Diagram 3.

Diagram 3 - Holdings of ordinary shares or voting stock

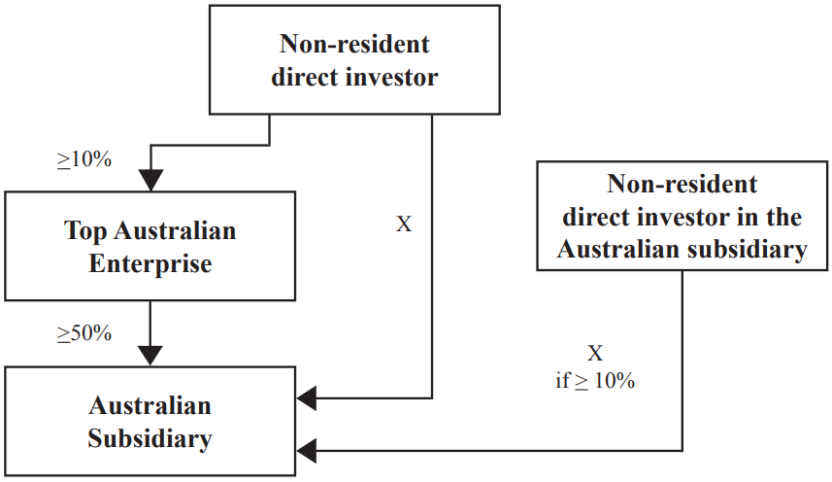

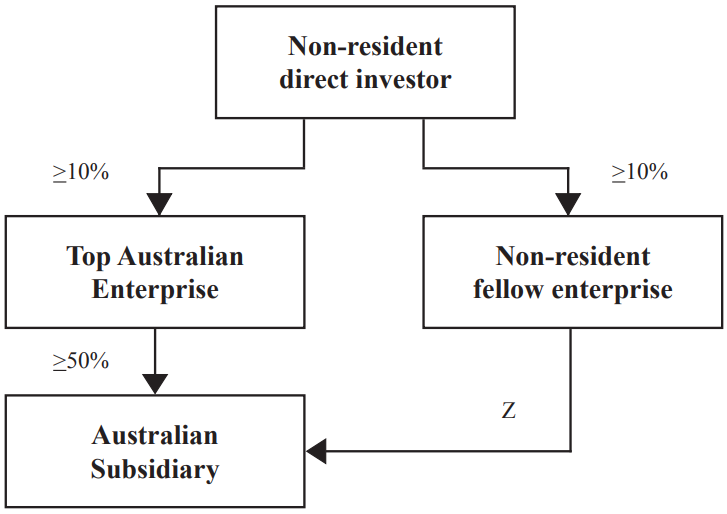

Direct investment groups abroad in Question 3a refers to any non-resident subsidiary, associate or branch of your Australian enterprise group (see Note 3.3) that holds 10% or more of the ordinary shares or voting stock in the Australian subsidiary.

For example, report all Y values in Diagram 4, where Y is 10% or more of the voting stock or ordinary shares in the Australian subsidiary. If Y is less than 10%, it should be reported in Q4.

Diagram 4 - Holdings of ordinary shares or voting stock

Fellow enterprises in Question 3a refers to any fellow enterprise of your Australian enterprise group that holds less than 10% of the ordinary shares or voting stock of the Australian subsidiary. For example, report all Z values in Diagram 5.

Diagram 5 - Holdings of ordinary shares or voting stock

B3 Other equity held by non-residents in this Australian subsidiary

Other equity held by non-residents in this Australian subsidiary refers to equity holdings of less than 10% of the ordinary shares or voting stock. Report holdings by your non-resident subsidiaries, associates and branches separate from other nonresident counterparties.

Including

- The source of funds for pooled investment funds managed by the Australian subsidiary (see Note 2).

- Non-residents on the shareholder register of the Australian subsidiary.

Part C Derivative contracts in a new liability position with non-residents

C1 Derivative contracts

Derivative contracts are agreements to buy or sell an asset at a future date at a price agreed today. They may relate to real or financial assets and may have a single or multiple settlement dates.

Including

- Forward foreign exchange

- Swaps, such as:

- Interest rate swaps

- Cross currency interest rate swaps

- Forwards and futures

- Options

- Other derivative contracts

C2 Derivative contracts in a net liability position with non-residents

Derivative contracts in a net liability position with non-residents are those contracts where the mark to market value of the closing position is negative at the reporting date.

Derivative contracts in a net asset position (positive mark to market value) at the end of the quarter should be reported in Question 16.

C3

The mark to market value of all derivatives in a net liability position at the end of the quarter should be reported as the closing position in Question 5. (Omit the negative sign.)

The opening position should be the closing position of the previous quarter, that is, the mark to market value of all derivatives in a net liability position at the end of the previous quarter.

The difference between opening and closing position should be reconciled in the same way as other questions. Report the settlements, market price changes and exchange rate changes of all contracts that are included in the closing position.

In addition, report the settlements, market price changes and exchange rate of all contracts that were settled (closed out) in a liability position during the quarter.

If there is a discrepancy remaining between opening and closing positions, this will be due to derivatives that have changed from asset to liability during the quarter or vice versa. Resolve this discrepancy by making the appropriate adjustment to market price changes.

C4

Settlements may occur on a net or gross basis, and should be reported accordingly.

Settlement receipts (credits) should include items such as:

- The receive leg of a contract in a net liability position

Settlement payments (debits) should include items such as:

- The payment at the maturity of a contract in a net liability position

- The payment leg of a contract in a net liability position

C5 Currency of outstanding amounts

For a derivative contract that involves the exchange of Australian dollars for a foreign currency, record that foreign currency.

For a contract that involves the exchange of two foreign currencies, record the currency that generates the net liability position. For example, in swapping US dollars for Japanese yen, if the market value of your yen payables exceeds the market value of your US dollar receivables, then a net yen liability position should be reported.

All figures should be converted to Australian dollars at the exchange rate on the reference date.

Part D Debt securities held by non-residents

D1 Short-term debt securities

Short-term debt securities include all debt securities issued by your Australian enterprise group which:

- Are held by non-residents

- Have an original contractual maturity of one year or less, and

- Are tradable in financial markets

Including

- Banker’s acceptances

- Certificates of deposit with contractual maturity of one year or less

- Notes issued under note issuance facilities (NIFs) and revolving underwriting facilities (RUFs)

- Repurchase agreements (Securities issued by your Australian enterprise group and loaned or otherwise provided under sale/buy back arrangements by your enterprise group to non-residents)

- Convertible and non-convertible securities

- Promissory notes

- Bills of exchange

- Other short-term commercial and financial paper

Excluding

- Derivatives, such as currency swaps or interest rate swaps used as a hedge against the security. (see Note 3.18)

- Australian securities held by the Australian office of a nominee on behalf of non-residents

Please report separately the securities held by non-resident direct investors, direct investment groups abroad, non-resident fellow enterprises and other non-resident counterparties.

Value all positions and transactions at market values rather than face values.

D2 Long-term debt securities

Long-term debt securities include all debt securities issued by your Australian enterprise group:

- Are held by non-residents

- Have an original contractual maturity of more than one year

- Are tradable in financial markets

Including

- Non-participating preference shares

- Bonds, including convertible bonds

- Asset-backed securities

- Repurchase agreements (Securities issued by your Australian enterprise group and loaned or otherwise provided under sale/buy back arrangements by your enterprise group to non-residents)

- Certificates of deposit with contractual maturity of more than one year

- Permanent debt security liabilities

- Other long-term securities

Excluding

- Derivatives, such as currency swaps or interest rate swaps used as a hedge against the security. (see Note 3.18)

- Australian securities held by the Australian office of a nominee on behalf of non-residents

Please report separately the securities held by non-resident direct investors, direct investment groups abroad, non-resident fellow enterprises and other non-resident counterparties.

- Value all positions and transactions at market prices rather than face values.

- Do not move securities from long term to short term as the residual maturity passes to less than one year.

Securities domiciled in Australia refers to those securities which were initially issued onto an Australian market and have since been acquired by non-residents.

D3 For depository corporations and investment funds

Debt securities held by affiliated depository corporations or investment funds are excluded from direct investment. This would include, for example, bonds issued by an Australian bank and held by a non-resident parent or subsidiary bank. Report debt securities issued by your Australian enterprise group and held by related depository corporations or investment funds under the Other non-resident counterparties category.

Part E Other financial liabilities to non-residents

E1 Trade credits and advances

Trade credits and advances are commercial credits extended to importers by exporters and prepayments made by importers to exporters. Trade credits should be reported at market value.

Trade credit and advances liabilities refer to accounts payable by your Australian enterprise group to non-residents for imports of goods and services and prepayments received from non-residents for future exports of goods and services.

Excluding

- Accounts payable due to transactions in financial assets or prepayments for transactions in financial assets. These should be reported in Question 13

- Payments arrears relating to financial assets, such as:

- Loan payments and interest arrears

- Derivative settlements arrears

These items should be reported against their relevant instrument even if they are past due.

E2 For depository corporations and investment funds:

Trade credit and other liabilities to affiliated depository corporations or investment funds are excluded from direct investment. This would include, for example, a trade credit from by a non-resident parent or subsidiary bank.

Report the liabilities of by your Australian enterprise group and held by related depository corporations or investment funds under the Other non-resident counterparties category.

E3 Loans

Loans include financial liabilities that are created through the lending of funds by a creditor (the non-resident investor) to a debtor (your Australian enterprise group) through an arrangement in which the lender receives a non-tradable document or instrument, or no security evidencing a transaction.

Question 9 collects details of loans from non-resident financial intermediaries.

Question 10 collects details of other loans from non-residents.

Use nominal (face) value as an approximation for market value unless book values have been revalued.

Including

- Advances, mortgages, bank overdrafts drawn, gold loans, financial leases and loans to finance trade

- Overdrawn nostro accounts

- Permanent debt loan liabilities

Excluding

- Unused standby credits and undrawn amounts of loans

E4 Deposit liabilities

Deposit liabilities can only be held by Authorised Deposit Taking Institutions (ADIs) regulated by the Australian Prudential Regulation Authority (APRA) under the Banking Act. Report deposits at nominal value unless book values have been changed.

Including

- Vostro accounts

- Gold accounts

Excluding

- Overdrawn vostro accounts. These should be reported as loans to non-residents in Question 20

- Bank account overdrafts drawn. These should be reported as loans liabilities or claims

- Certificates of Deposit. These should be reported as debt securities in either Question 6 or Question 7

E5 Transferable deposits

Transferable deposits comprise of all deposits that are:

- Exchangeable for banknotes and coins, of any currency, on demand and at par without any penalty or restriction

- Directly usable for making payments by cheque, draft, giro order, direct debit/credit, or other direct payment facility, without any penalty or restriction

E6 Other liabilities

Other liabilities include miscellaneous accounts payable and any items not classified as loans or trade credits. Other liabilities should be reported at market value.

Including

- Accounts payable due to transactions in financial assets or prepayments for transactions in financial assets

- Derivative margin account liabilities

Section 2: Claims on non-residents

Part F Equity held in non-resident enterprises

F1 Equity

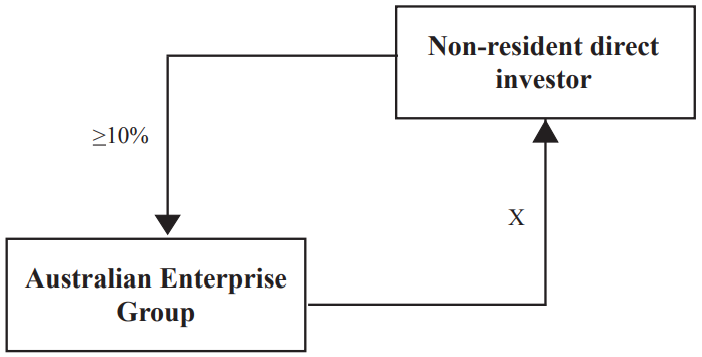

Equity held by your Australian enterprise group in your non-resident direct investors, Question 15, comprise your reciprocal ownership interests in non-resident direct investors. For example, report all X values in Diagram 6.

Your holdings of less than 10% of the issued capital of these investors should be reported separately to your holdings of 10% or more of their total issued capital. Equity positions should be reported at market value.

Excluding

- Non-participating preference shares (see Note F6)

Diagram 6 - Holdings of ordinary shares or voting stock

F2 Transactions that increase or decrease your equity assets held in non-resident enterprises

Including

- Purchases or sales of shares held in non-resident enterprises

- Non-bonus issues, including calls and dividends re-invested

- Redemptions of shares in non-resident enterprises

- Additions and withdrawals of equity capital by the Australian head office

Excluding

- Dividends received

- Remitted profits (see Note 3.13)

F3 After tax operating profit

After tax operating profit attributable on your direct investment refers to the consolidated operating profit (see Note 3.12) less tax payable on income earned during the quarter attributable on your portion of the equity of the enterprise.

For example, should the top non-resident enterprise own 80% of the ordinary shares of a subsidiary which in turn owns 60% of the ordinary shares of a subsidiary, then the percentage of ordinary shares which the top enterprise owns in the second subsidiary is calculated as 80% of 60% i.e. 48%.

If exact values are not available, careful estimates will suffice.

F4 Other equity held in non-resident enterprises

Other equity held in non-resident enterprises, Question 15, refers to equity held by your Australian enterprise group in non-residents who are not direct investors in your group.

Direct investment groups abroad in Question 15 refers to the equity claims on your non-resident subsidiaries, associates and branches.

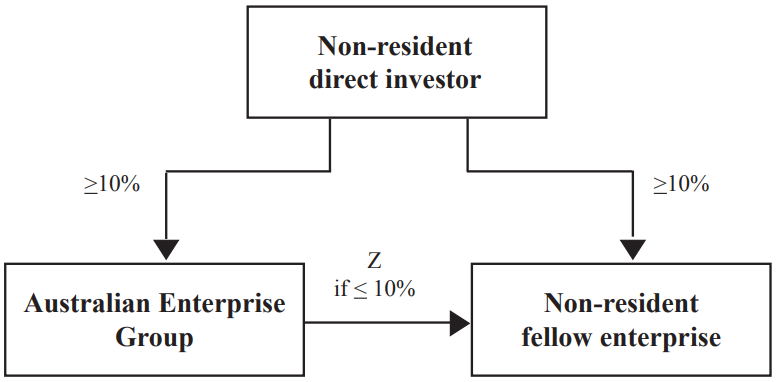

Non-resident fellow enterprises in Question 15 refers to equity claims on non-resident enterprises which share a common direct investor as your Australian Enterprise Group. For example, report all Z in Diagram 7.

Diagram 7 - Holdings of ordinary shares or voting stock

Other non-resident counterparties in Question 15 refers to claims on unrelated nonresident enterprises that are less than 10% of the ordinary shares or voting stock of that enterprise. Equity positions should be reported at market value (see Note F5).

Including

- Shares held in non-resident enterprises that are listed on the Australian stock exchange

- Depository receipts (e.g. American depository receipts)

- Units in non-resident pooled investment funds (see Note 2)

- Shares acquired under stock-lending arrangements where your Australian enterprise group becomes the registered holder of the shares

Excluding

- Non-participating preference shares (see Note F6)

- Shares held by your Australian enterprise group in related enterprise.

F5 Market value of equity

For listed enterprises, equity positions should be reported using the market price on the reference date.

For unlisted enterprises if a market price is not available, please estimate the market value of your shares by using one of the following methods, which are listed in order of preference:

- A recent transaction price

- Director’s valuation

- Net asset value

Net asset value is equal to total assets less non-equity liabilities, including intangibles. Assets and liabilities should be recorded at estimated market value, rather than historical values.

For net equity of a branch, joint venture or other unincorporated enterprise, report the total assets of the branch valued at current cost, less non-equity liabilities. Equity liabilities include retained earnings revaluation and other reserves, as well as capital invested by the head office.

F6 Non-participating preference shares

Non-participating preference shares are a type of preference share where the holder has no entitlement to a share in the residual value on the dissolution of the issuing entity. Non-participating preference shares should be reported as ‘Long-term debt securities’ in Question 18.

F7 Equity in the form of securities

Equity in the form of securities refers to any equity you hold that is denominated in the form of listed or unlisted securities. This qualification is only relevant where the equity holding is less than 10% of the voting rights of the enterprise.

Part G Derivative contracts in a net asset position with non-residents

G1 Derivative contracts

Derivative contracts are agreements to buy or sell an asset at a future date at a price agreed today. They may relate to real or financial assets and may have a single or multiple settlement dates.

Including

- Forward foreign exchange

- Swaps, such as:

- Interest rate swaps

- Cross currency interest rate swaps

- Forwards and futures

- Options

- Other derivative contracts

G2 Derivative contracts in a net asset position with non-residents

Derivative contracts in a net asset position with non-residents are those contracts where the mark to market value of the closing position is positive at the reporting date.

Derivative contracts in a net liability position (negative mark to market value) at the end of the quarter should be reported in Question 5.

G3

The mark to market value of all derivatives in a net asset position at the end of the quarter should be reported as the closing position in Question 16.

The opening position should be the closing position of the previous quarter, that is, the mark to market value of all derivatives in a net asset position at the end of the previous quarter.

The difference between opening and closing position should be reconciled in the same way as other questions. Report the settlements, market price changes and exchange rate changes of all contracts that are included in the closing position.

In addition, report the settlements, market price changes and exchange rate of all contracts that were settled (closed out) in an asset position during the quarter.

If there is a discrepancy remaining between opening and closing positions, this will be due to derivatives that have changed from asset to liability during the quarter or vice versa. Resolve this discrepancy by making the appropriate adjustment to market price changes.

G4 Settlements

Settlements may occur on a net or gross basis, and should be reported accordingly.

Settlement payments (debits) should include items such as:

- The payment of a contract in a net asset position

Settlement receipts (credits) should include items such as:

- The receipt at the maturity of a contract in net asset position

- The receive leg of a contract in net asset position

G5 Currency of outstanding amounts

For a derivative contract that involves the exchange of Australian dollars for a foreign currency, record that foreign currency.

For a contract that involves the exchange of two foreign currencies, record the currency that generates the net asset position. For example, in swapping US dollars for Euros, if the market value of your Euro receivables exceeds the market value of your US dollar payables, then a net Euro asset position should be reported.

All figures should be converted to Australian dollars at the exchange rate on the reference date.

Part H Debt securities issued by non-residents

H1 Short-term debt securities

Short-term debt securities include all debt securities held by your Australian enterprise group which:

- Were issued by non-residents

- Have an original contractual maturity of one year or less, and

- Are tradeable in financial markets

Including

- Treasury notes

- Banker’s acceptances

- Certificates of deposit with contractual maturity of one year or less

- Debt securities acquired under repurchase or stock lending arrangements

- Notes issued under note issuance facilities (NIFs) and revolving underwriting facilities (RUFs)

- Convertible and non-convertible securities

- Promissory notes

- Bills of exchange

- Other short-term commercial and financial paper

Excluding

- Derivatives, such as currency swaps or interest rate swaps used as a hedge against the security. (see Note 3.18)

Please report separately the securities issued by non-resident direct investors, direct investment groups abroad, non-resident fellow enterprises and other non-resident counterparties.

Value all positions and transactions at market prices rather than face values

H2 Long-term debt securities

Long-term debt securities include all debt securities issued by non-residents and held by your Australian enterprise group which have an original contractual maturity of more than one year and are tradable in financial markets.

Including

- Non-participating preference shares

- Bonds, including convertible bonds

- Asset-backed securities

- Debt securities acquired under repurchase or stock lending arrangements

- Certificates of deposit with contractual maturity of more than one year

- Permanent debt security liabilities

- Other long-term securities

Excluding

- Derivatives, such as currency swaps or interest rate swaps used as a hedge against the security. (see Note 3.18)

Please report separately the securities issued by non-resident direct investors, direct investment groups abroad, non-resident fellow enterprises and other non-resident counterparties.

- Value all positions and transactions at market prices rather than face values.

- Do not move securities from long term to short term as the residual maturity passes to less than one year.

H3 For depository corporations and investment funds:

For depository corporations and investment funds: Debt securities issued by affiliated depository corporations or investment funds are excluded from direct investment. For example, bonds issued by a non-resident parent and held by the Australian bank or branch.

Report debt securities issued by related depository corporations or investment funds and held by your Australian enterprise group under the Other non-resident counterparties category.

Part I Other financial claims on non-residents

I1 Trade credits and advances

Trade credits and advances are commercial credits extended to importers by exporters and prepayments made by importers to exporters. Trade credits and advances should be reported at market value.

Trade credits and advances claims refer to accounts receivable by your Australian enterprise group from non-residents for exports of goods and services and prepayments made by your Australian enterprise group for future imports of goods and services.

Excluding

- Accounts receivable due to transactions in financial assets or prepayments for transactions in financial assets.

- Payments arrears relating to financial assets, such as:

- Loan interest arrears

- Derivative settlements arrears

These items should be reported against their relevant instrument even if they are past due.

Accounts taken over by the Export Finance Insurance Corporation should be treated as paid.

I2 For depository corporations and investment funds:

Trade credit and other claims on affiliated depository corporations or investment funds are excluded from direct investment. This would include, for example, a trade credit claim on a non-resident parent or subsidiary bank.

Report the claims of by your Australian enterprise group and held by related depository corporations or investment funds under the Other non-resident counterparties category.

I3 Loans

Loans include financial assets that are created through the lending of funds by a creditor (your Australian enterprise group) to a debtor (non-residents) through an arrangement in which the lender receives a non-tradable document or instrument, or no security evidencing a transaction.

Question 20 collects details of loans to non-resident financial intermediaries. Question 21 collects details of other loans to non-residents.

Use nominal (face) value as an approximation for market value, unless book values have been revalued.

Including

- Advances, mortgages, finance leases and loans to finance trade

- Permanent debt loan claims

- Deposit overdraft claims on non-residents, if your Australian enterprise group is an Authorised Deposit Taking Corporation (ADI)

- Overdrawn vostro accounts

Excluding

- Unused standby credits and undrawn amounts of loans

I4 Deposit claims

Deposit claims can only be against a counterparty that is financial intermediary, such as a bank. Use nominal (face) values unless book values have been revalued.

Including

- Nostro accounts

- Gold accounts where you have a claim against a non-resident institution for the delivery of gold or its equal value

Excluding

- Overdrawn nostro accounts. These should be reported as loans from non-residents in Question 9

- Deposit account overdrafts:

- Drawn by you. These should be reported as loan liabilities in Question 9

- Drawn against you by your clients. These should be reported as loans to non-residents in Question 20

- Certificates of Deposit. These should be reported as debt securities in either Question 17 or Question 18

- Gold where title is held directly by your Australian enterprise group and the physical gold is held but not owned by a third party.

Transferable deposits comprise of all deposits that are:

- Exchangeable for banknotes and coins, of any currency, on demand and at par without any penalty or restriction

- Directly usable for making payments by cheque, draft, giro order, direct debit/ credit, or other direct payment facility, without any penalty or restriction

I5 Foreign currency note and coin holdings of your Australian enterprise group

Foreign currency note and coin holdings of your Australian enterprise group refers to the cash holdings of foreign currency notes and coins held by your Australian enterprise group. Foreign currency bank accounts should be reported with your deposit claims in Question 22.

Excluding

- Gold and gold accounts.

I6 Other claims

Other claims include overdue settlements (or amounts past due and unpaid), miscellaneous accounts receivable and any items not classified as loans and trade credits. Other claims should be reported at market value.

Including

- Accounts receivable due to transactions in financial assets or prepayments for transactions in financial assets

- Derivative margin account claims

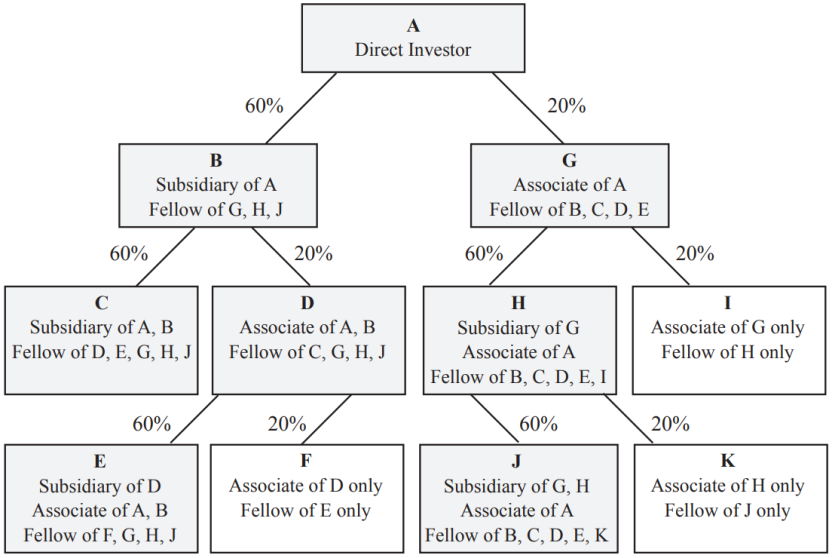

Appendix 1: Direct investment relationships

X.1 A direct investment relationship

A direct investment relationship is established when an enterprise that is resident in one country holds 10% or more of the ordinary shares or voting stock of an enterprise resident in another country. The ‘parent’ entity is a direct investor, the ‘child’ entity is a direct investment enterprise.

The direct investment relationship extends to all enterprises related to the direct investor, both ‘parents’ and ‘children.’ For the purpose of the Survey of International Investment, related enterprises in a direct investment relationship are as follows.

Identifying related enterprises in a direct investment relationship

Diagram X1 shows chains of ownership which illustrate the concept of subsidiaries, associates, branches and fellows comprising a group of enterprises related to a direct investor. The distinctions made are influence and control. Non-resident enterprises over which you have either influence or control are considered to be part of your direct investment group abroad. A non-resident enterprise that has influence or control over your Australian Enterprise group are considered to be part of your director investment group in Australia.

Diagram X1 - Assume enterprise A has the following investments, with ownership of ordinary shares or voting stock as indicated:

X.2 Subsidiaries

Subsidiaries are enterprises wholly or majority owned by an investor. The direct investor has control over a subsidiary though its majority holding.

Enterprise B is a subsidiary of enterprise A as,

- Enterprise A owns more than half of the voting power in B. A is considered to have control over B.

Enterprise C is a subsidiary of enterprise A as,

- Enterprise C is a subsidiary of enterprise B, which is a subsidiary of enterprise A. A has control over C through its control over B.

X.3 Associates

Associates are enterprises in which a direct investor or its subsidiaries owns greater than 10% but less than 50% of ordinary shares or voting stock. The direct investor has influence over an associate but not control.

- Subsidiaries of associates are considered to be associates of the direct investor.

- Associates of subsidiaries are considered to be associates of the direct investor.

- Associates of associates are not considered to be related to the direct investor.

Enterprise G is an associate of Enterprise A as:

- Enterprise A holds between 10% and 50% or more of the voting power in G. A has influence over G but not control.

Enterprise D is an associate of Enterprise A as:

- Enterprise B is a subsidiary of enterprise A and B holds between 10% and 50% of the voting power in D. B has influence over D and A has control over B, therefore A has influence over D through its control over B.

Enterprise J is an associate of Enterprise A as:

- Enterprise J is a subsidiary of Enterprise H, which is an associate of A. As H has control over J, A can use its influence in H to influence J..

Enterprise I is not an associate of Enterprise A as:

- Enterprise A owns less than 50% of enterprise G and enterprise G owns less than 50% of enterprise I. While A has influence over G and G has influence over I, any influence A has over I is considered to be diluted by the two minority holdings.

An associate of an associate is not considered to be under the influence of the ultimate parent, even if the parent’s holding of the voting rights in the associate of associate is greater than 10%.

X.4 Branches

Branches are unincorporated enterprises wholly or jointly owned by an investor. Branches are treated as notional subsidiaries for the purposes of Form 90.

X.5 Fellow enterprises

Fellow enterprises have the same direct investor but are not directly related subsidiaries, associates or branches of each other. Fellow enterprises have a ‘common parent,’ which may lead to preferential dealing between fellows.

Enterprise B is a fellow of Enterprise G as:

- Both B and G are subsidiaries or associates of enterprise A, but neither B nor G hold greater than 10% of ordinary shares or voting stock in each other. A has either influence or control over both B and G. A is a common direct investor shared by both B and G

Enterprise H is a fellow of Enterprise I as:

- Both H and I have G as a common direct investor, but neither hold more than 10% in the other.

Enterprise I is not a fellow of Enterprise B as:

- I is not an associate of A due to the dilution of influence by the two minority holding of I by G and of G by A. Therefore B and I do not have a common direct investor in A.

The enterprises shaded in grey in Diagram 1 are considered to be part of A’s direct investment group abroad. As A has either influence or control over all the shaded enterprises, these enterprises may grant each other preferential deals. Note that the direct investment groups of the enterprises under A differ to the direct investment groups of A itself.

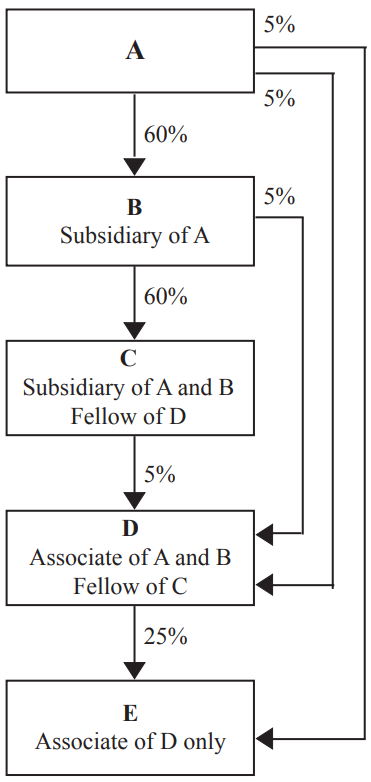

X.6 Combined equity positions

The conceptual relationships defined above are also considered in combinations. Assume Enterprise A has the following holdings of ordinary shares or voting stock:

Diagram X2 - Direct investment relationships with a combination of investors

Equity holdings of subsidiaries are combined to define relationships. Enterprise A is considered to have influence over Enterprise D because its immediate ownership of voting power in combination with its control over B and C give A 15% of the voting power in D. D is an associate of A. For the same reason, D is also an associate of B.

C and D are fellow enterprises as C holds less than 10% of D and both C and D share A as a common direct investor.

A and E are considered to be unaffiliated: A is not a direct investor in E. As A only has influence, not control, over D, the holding of voting power of D in E is not combined with A’s holding of voting power.